After years of lacklustre performance caused by a series of debt and currency crises, Europe became a major contributor to the global economic resurgence in 2017. The region achieved a broad-based economic recovery with GDP growth of over 2.0%, among its highest GDP growth rates in a decade. Hastened by strong business and consumer confidence, many industries prospered in 2017, further supporting the multiplier effect in trade and industrial production. In particular, the aviation sector posted one of its strongest year-over-year gains ever.

Expansion in international traffic on long-haul segments between Europe and other regions such as Asia and the Middle East was also apparent in 2017. Growing impetus for the long-haul low-cost business model, especially on transatlantic segments, represented an important industry evolution. The blurring or hybridization of business models between traditional full-service carriers and low-cost carriers continues to be an important development in the industry, especially in European markets. As a symptom of this new, game-changing environment, 2017 saw a significant number of airline bankruptcies and a wave of consolidation. At the same time, continued inroads by incumbent low-cost carriers in the intra-European market such as Ryanair, easyJet, Wizz Air and Jet2, among others, show the resilience of this business model in certain market segments. Within Europe, routes linking London Gatwick (LGW) and Paris Orly (ORY) with Spanish destinations such as Barcelona (BCN) demonstrated both high traffic volume and significant year-over-year growth. The long-haul route between London Heathrow (LHR) and Hong Kong (HKG) continues to experience robust traffic.

Despite the reassurance provided by strong macro-economic fundamentals, uncertainty and downside risks for the European single aviation market remain a major concern leading into 2019. The UK’s exit from the EU begs the question of what impact changes in that large aviation market will have on the European market and aviation in general. Irrespective of these downside risks, the UK achieved 5.9% air passenger traffic growth in 2017, well above its average annual growth over the last decade. In fact, an analysis of Europe’s top 20 country markets shows that median growth in 2017 was 8.2%, which is above the compounded annual growth rate of 4% for Europe as a whole. After weak traffic numbers in 2016, Turkey (+11.2%) and Russia (+16.7%), respectively the fourth- and fifth-largest European markets in 2017, recorded notable rebounds.

Eastern Europe’s record-breaking growth

Airports located in Western and Southern Europe continue to handle a significant proportion of European passenger traffic. These sub-regions accounted for 64% of the continent’s traffic; their average growth rates since 2000 have been 2.8% and 4.8% per annum respectively.

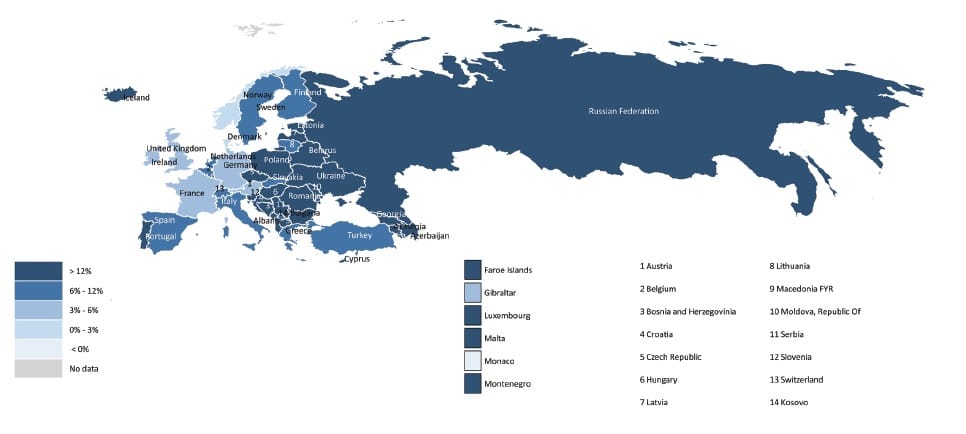

Eastern Europe is turning into a major player in the region, however. Although the sub-region only represented slightly more than 14% of Europe’s total traffic in 2017, record growth in its air transport industry is gradually increasing its countries’ importance in the continental market. Eastern Europe’s airports have achieved the highest average annual passenger traffic growth in Europe this century. From 2000 to 2017, airports in Eastern Europe achieved average growth rates of over 10.1% per annum, as noted in Chart 2. This is largely attributable to the fast growth of major commercial airports in Russia, but other burgeoning markets – such as Poland, Romania and Ukraine – have become contributors to this growth. Passenger traffic growth between 2016 and 2017 reached double-digit for every single country in the sub-region.

Revival in European air cargo

Before 2016, the region’s air cargo market had experienced very little change in overall volume since 2010, which coincided with the rebound after the Great Recession. While 2016 was considered a recovery year, 2017 saw an 8.6% increase, one of the largest volume growth rates of all regions. Many of Europe’s major air cargo hubs saw significant volume gains in 2017, well above their average annual growth rates for the past 20 years. Certainly, a weakened Euro against the U.S. dollar and Chinese Yuan helped bolster external demand for cargo shipped from the monetary union.

Germany, Europe’s largest economy and manufacturing centre, handled the highest proportion of the region’s air cargo. Volume handled by the country’s airports grew 6.7% to 4.9 million tonnes of air cargo. Even cargo volume from the UK, which continues to be spooked by the uncertainty surrounding Brexit, leapt 9.1%. Air cargo grew 2.1% on an annual basis from 2000 to 2017, as seen in Chart 3. Turkish airports in particular saw the greatest gains and in 2017 achieved 20.4% growth, one of Turkey’s largest year-over-year increases. In 2016, Turkish airports saw overall volume rise 14.7%, which indicates that throughout the period air cargo flows were less sensitive to geopolitical and security concerns than was passenger traffic. Other major air cargo countries which achieved double-digit-percentage gains were Spain (+14.1%), Luxembourg (+12.0%), Russia (13.2%) and Switzerland (+10.7%).

Europe Outlook 2018 – Robust growth in 2018’s first half amidst downside risks

Europe maintained its robust growth trend through the first half of 2018, achieving 6.7% growth for the six months. Although the current trend points toward a slowdown in the second half of the year, overall growth for the year should be above 5%. A developing trend in the region for 2018 is the emergence of peripheral countries (in Eastern and Southern Europe, as well as the Baltic States) as major growth centres for European aviation. The increasing prevalence of low-cost carriers in those markets, together with improving economic conditions, have propelled the European market significantly in the recent year. Even though a backdrop of uncertainty is hanging over the aviation market, brought on by the prospective withdrawal of the UK from the European Union, aviation in Europe should remain unfettered in the short term.

The UK, Europe’s largest aviation market, experienced subdued growth in the first half of 2018. Although the UK market grew by a robust 5.9% in 2017, its growth slowed to 2.2% in this year’s first six months. UK GDP is projected to grow 1.6% by the end of the year, below France and Germany’s respective 2.1% and 2.5% projected rates. As difficult negotiations on the details of the UK’s exit from the EU continue, the country is still facing a high degree of economic uncertainty.

Spain’s passenger market grew 6.8% in the first half of 2018. The country’s domestic segment, which represents about a third of its total market, drove much of the increase, growing 11.8%. The international segment also grew during the period, but at a more moderate 4%. Madrid Airport (MAD) had a particularly good run up to June, its traffic growing 8.2% in the year’s first six months.

German airports’ passenger traffic grew at the same 2.2% pace as did the UK airports in the first half of 2018. The country’s domestic segment saw traffic decline during the period, following a particularly strong year in 2017. The collapse of Air Berlin was responsible for the domestic passenger traffic decline. Dusseldorf Airport (DUS) typified the trend, its domestic traffic falling 13.2% over the six months, contributing to an 8% decline in its total passenger traffic for the period. Frankfurt Airport (FRA) escaped the domestic traffic downturn unscathed, thanks to the continued strength of its inter-European traffic, and posted a 9.1% traffic increase for the period.

Turkey’s passenger market suffered major setbacks in 2016 but managed to start recovering momentum in early 2017. The country’s major airports saw their combined passenger traffic grow 16% in the first half of 2018. Turkey’s three largest airports, located in Istanbul and Antalya, surged during the period, growing 12.9% (IST), 12.4% (SAW) and 25.2% (AYT) respectively. Recent news regarding the national economy leave the second half of the year under a cloak of uncertainty, however. The Turkish lira has tumbled in international markets as inflationary pressure remains on the rise.

The Russian Federation’s GDP growth is set to rebound this year after a two-year contraction. The country’s passenger market had already begun recovering in 2017, growing 16.7% for the year, and grew another 11.1% in the first half of 2018. Given the current passenger traffic growth trend in Eastern Europe, against a backdrop of a macroeconomic recovery and slowly rising commodity prices, there is a good chance the Russian Federation’s traffic growth for the full year of 2018 will remain in the double digits.

France gained more ground in the first half of 2018 than its regional peers Germany and the U.K., posting 4.1% traffic growth for the period. Among the major European markets, Italy performed relatively well in the first half of 2018, its traffic growing 6.1%. Milan’s Malpensa Airport (MXP) provided a significant portion of this growth, achieving 11.1% growth for the first half of the year.

For more detailed analysis and insights on air transport demand, please peruse ACI’s suite of products. With comprehensive data coverage for over 2,500 airports in 175 countries worldwide, ACI’s World Airport Traffic Report remains the authoritative source and industry reference for the latest airport traffic trends, rankings and data rankings on air transport demand. Boasting traffic forecasts for over 100 country markets, the World Airport Traffic Forecasts (WATF) dataset presents detailed metrics which include total number of passengers (broken down into international and domestic traffic), total air cargo and total aircraft movements. Absolute figures, compounded annual growth rates (CAGR), market shares and global growth contributions are presented over three time horizons: short-, medium- and long-term over the 2017–2040 period.

comments