Drawing on global data from the 2026 Airport Economics Report and Key Performance Indicators, and insights from the recent Trinity Forum, this article examines the evolving state of airport non-aeronautical business and the megatrends shaping future airport commercial strategy.

Key Insight

Global passenger traffic rebounded in 2024, but commercial revenues still lag, highlighting the need for airports and their partners to reinvent how commercial value is captured.

“Growth comes from better recipes, not just more ingredients.”

— Paul Romer, Nobel Laureate in Economics

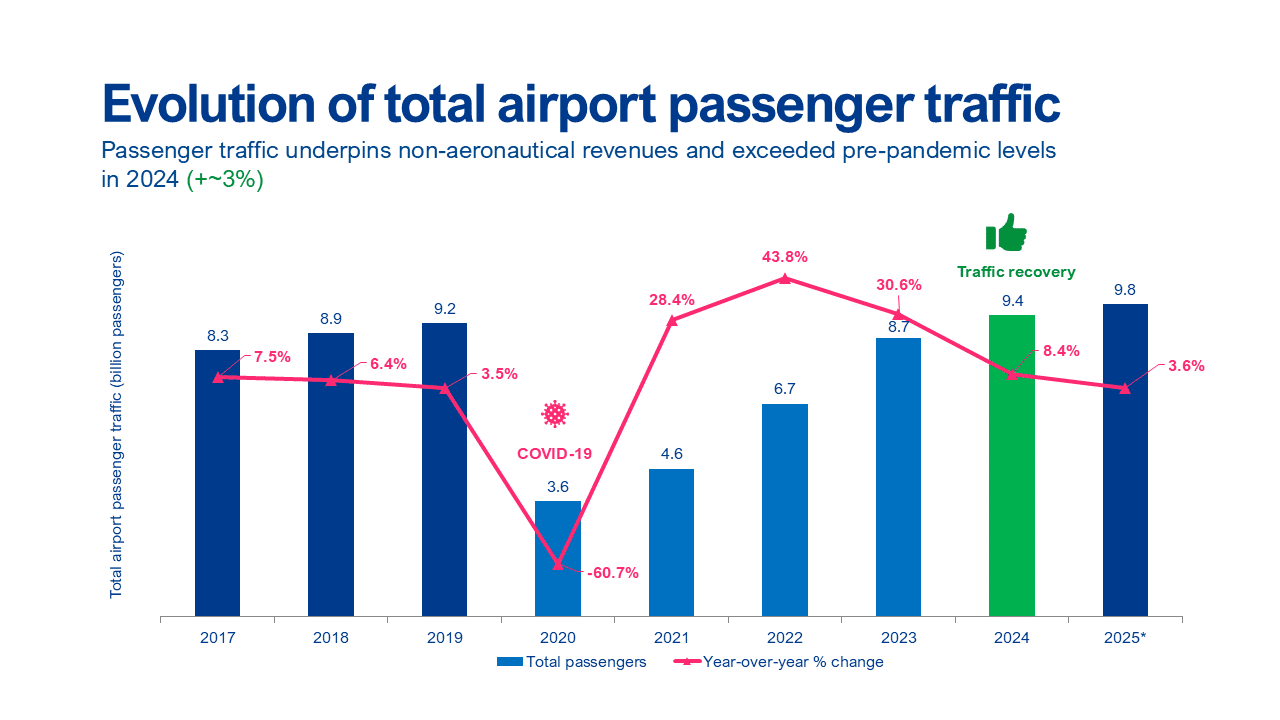

Passenger Traffic Underpins Non-Aeronautical Revenues

Passenger traffic remains the fundamental driver of airport economics, particularly non-aeronautical revenues.

In 2024, global passenger volumes reached 9.4 billion, exceeding pre-pandemic levels by approximately 3%. Following the unprecedented contraction of -60.7% in 2020, traffic rebounded strongly through 2022 and 2023 and fully recovered in 2024.

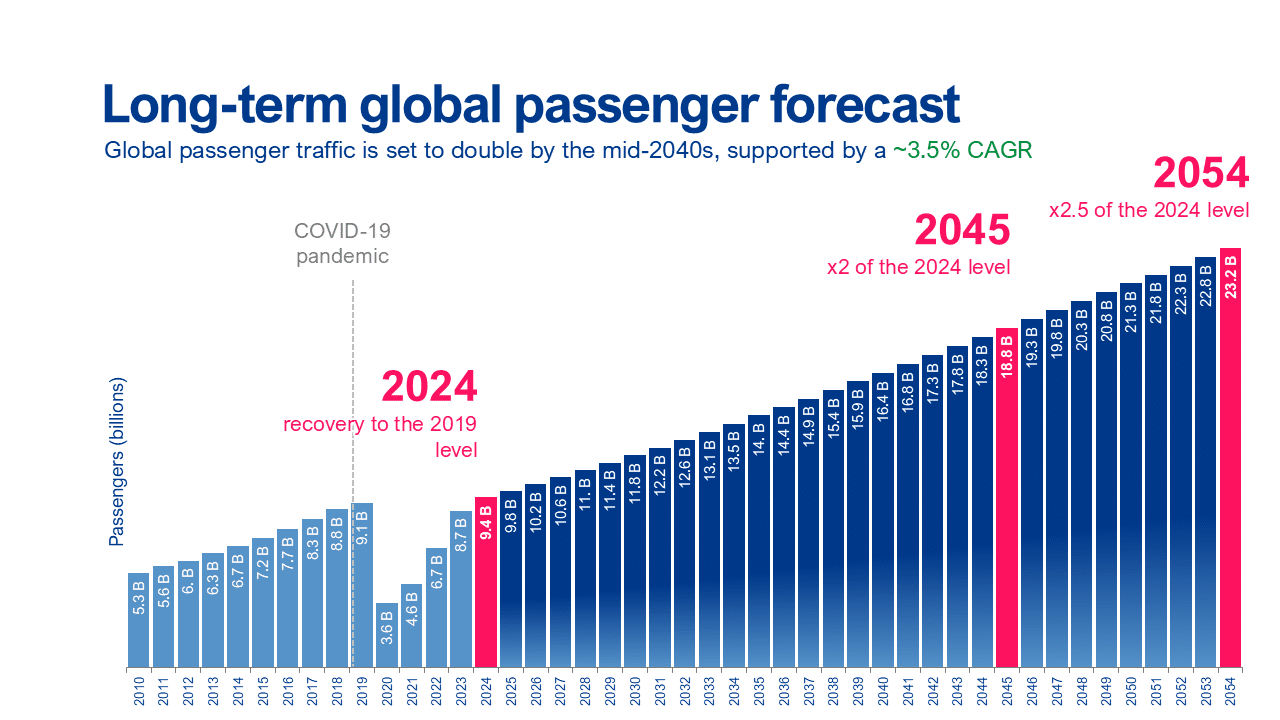

The long-term outlook remains robust. Global passenger traffic is projected to double by the mid-2040s, supported by an estimated ~3.5% compound annual growth rate.

Passenger growth is once again providing the volume base for commercial activity. The challenge lies in translating that growth into sustainable revenue performance.

What Are Airport Non-Aeronautical Revenues?

Airport non-aeronautical revenues are the commercial income airports generate from activities not directly related to airline operations. These include retail concessions, food and beverage, car parking, property and real estate, advertising, and other passenger services.

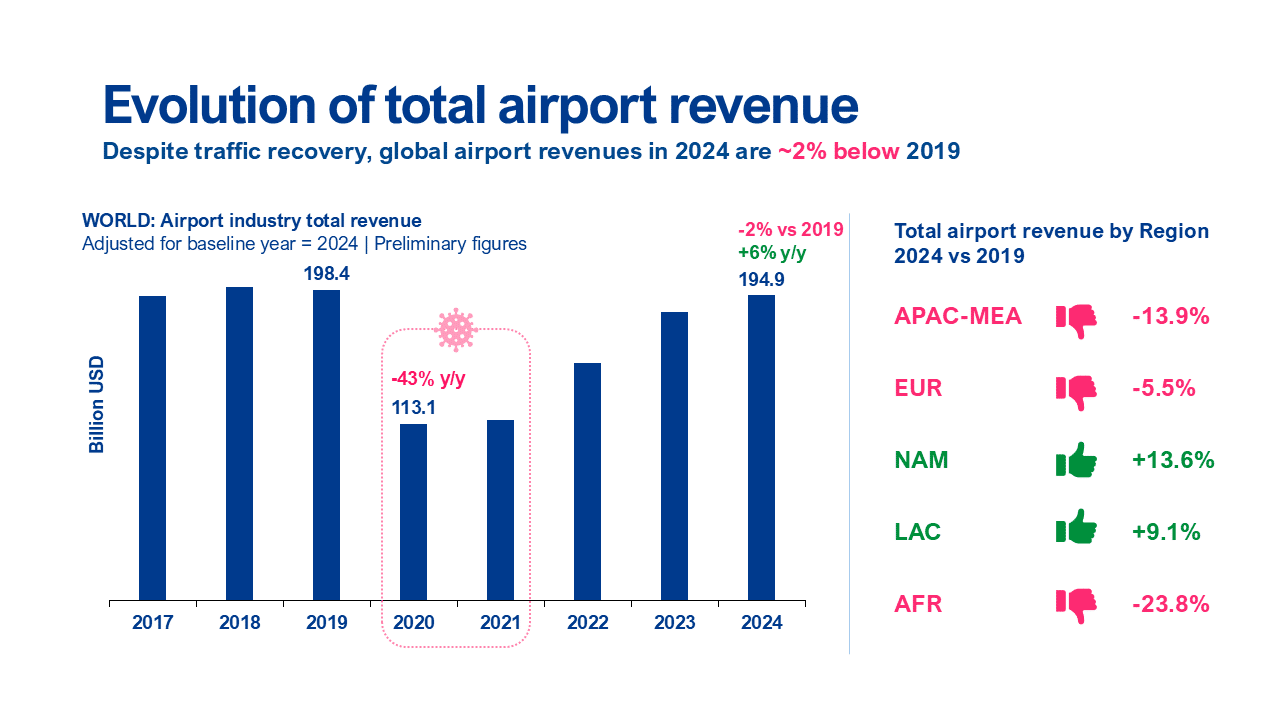

Airport Revenue Recovery Lags Passenger Traffic Recovery

Despite passenger traffic exceeding 2019 levels, total airport revenues in 2024 remain approximately 2% below pre-pandemic benchmarks globally.

Regional performance illustrates the uneven pace of recovery:

- North America: +13.6% above 2019 levels

- Latin America: +9.1% above 2019 levels

- Europe: -5.5%

- APAC–MEA: -13.9%

- Africa: -23.8%

Passenger recovery has been broad-based. Revenue recovery has been differentiated across regions.

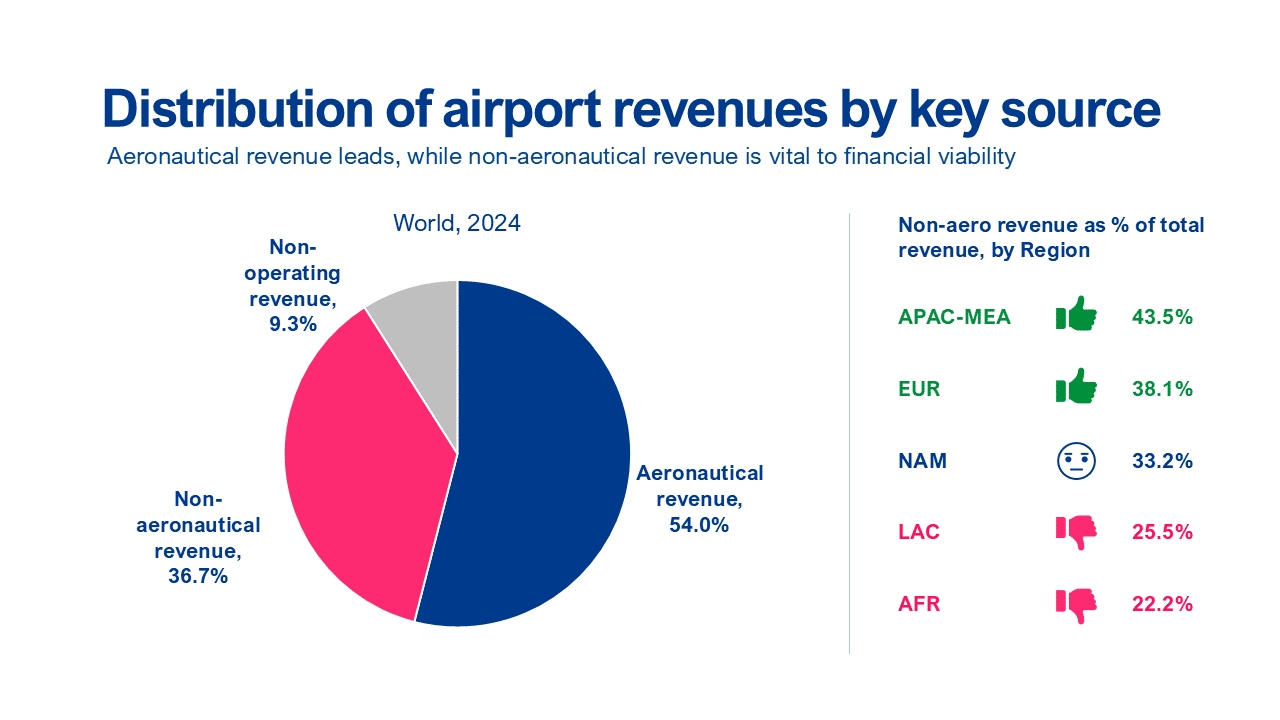

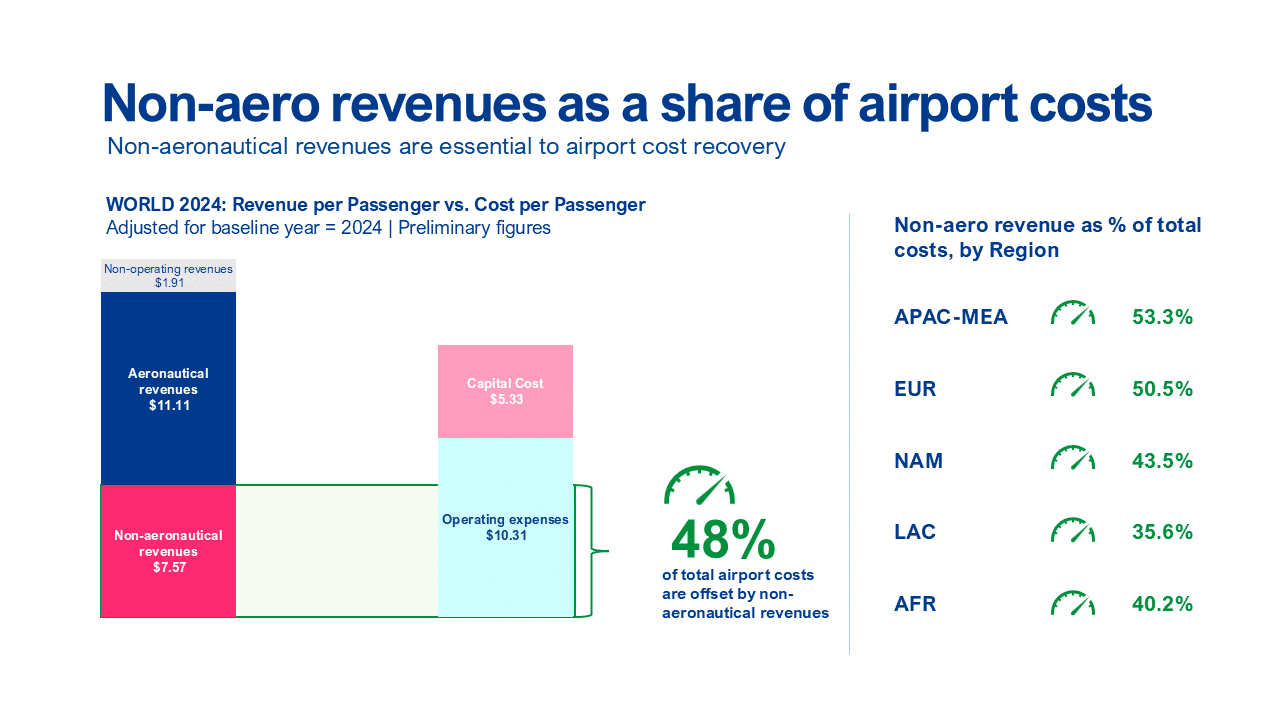

Why Non-Aeronautical Revenues Are Critical to Airport Financial Viability and Cost Recovery

Airports are highly competitive businesses in their own right, generating revenues from two main sources: aeronautical activities and non-aeronautical, or commercial, activities.

The revenue structure of airports highlights the structural importance of commercial activity. Globally, non-aeronautical revenues account for 36.7% of total income, rising to 43.5% in APAC–MEA and 38.1% in Europe. Even in regions with lower shares, non-aeronautical revenues remains a substantial component of airport revenues.

Their significance becomes clearer when viewed against costs. Globally, non-aeronautical revenues offset 48% of total airport costs, exceeding 50% in APAC–MEA and Europe.

On a per-passenger basis in 2024:

- Non-aeronautical revenue: USD 7.57

- Operating expenses: USD 10.31

- Capital costs: USD 5.33

Commercial revenues are therefore not supplementary – they are fundamental to airport financial sustainability.

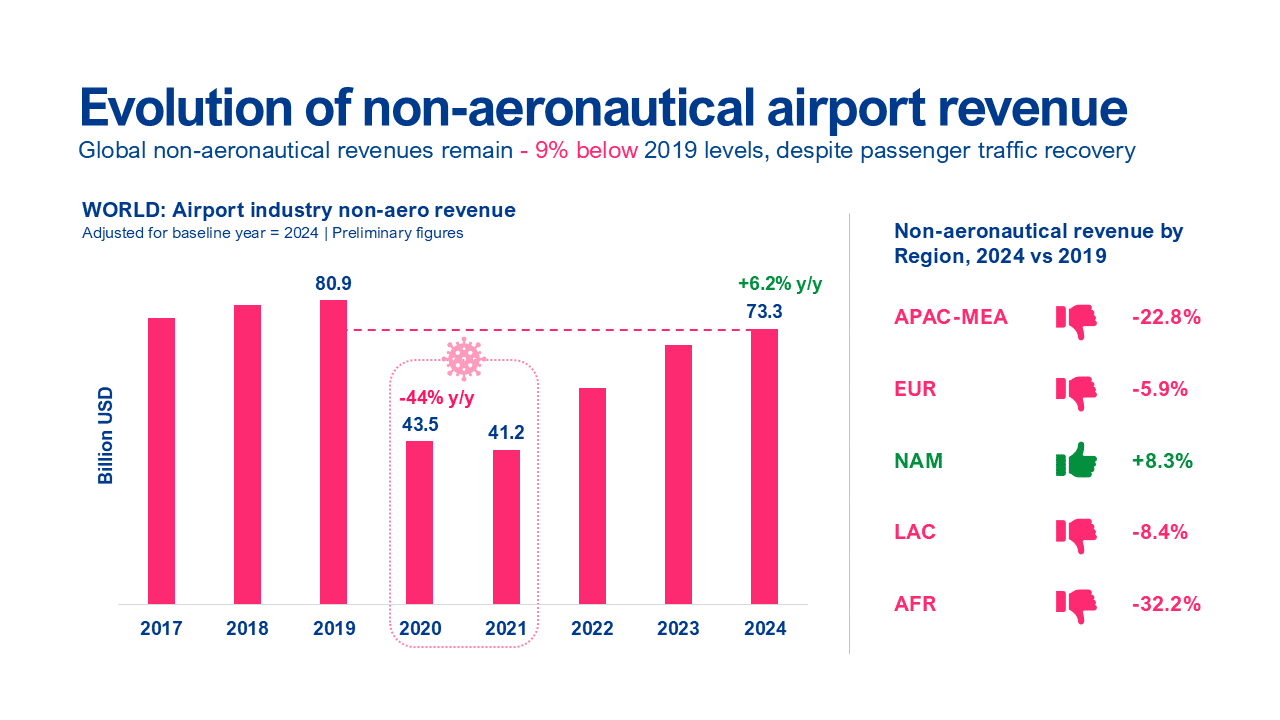

Non-Aeronautical Revenue Recovery Remains Uneven

Globally, non-aeronautical revenues remain approximately 9% below 2019 levels, despite full passenger recovery. North America has moved above its pre-pandemic benchmark, while Europe remains slightly below. In APAC–MEA and Africa, the recovery gap remains materially wider, and Latin America continues to close the gap more gradually.

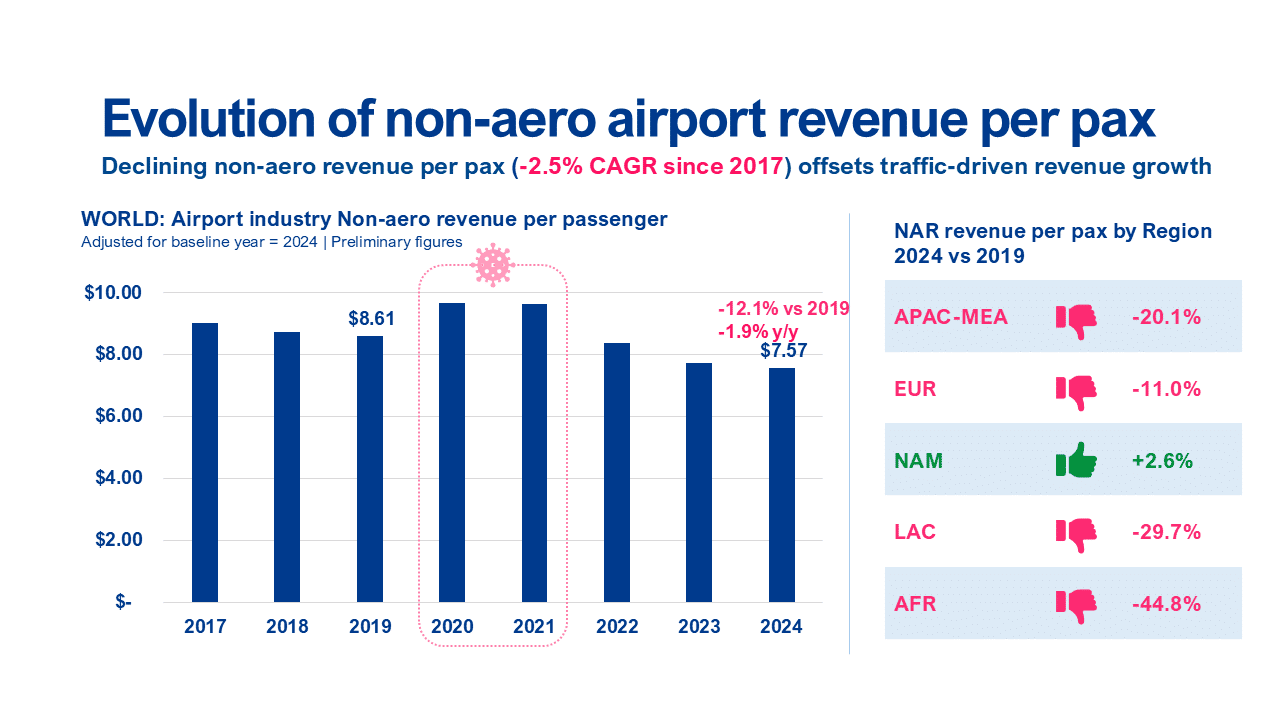

The divergence becomes more pronounced when measured per passenger. Non-aeronautical revenue per passenger declined from USD 8.61 in 2017 to USD 7.57 in 2024 — a reduction of roughly 12% compared to 2019 and a negative CAGR of about –2.5% over the period.

North America shows relative stability in revenue per traveller, whereas Europe and APAC–MEA exhibit more noticeable compression. In Latin America and Africa, the decline in revenue per passenger is sharper.

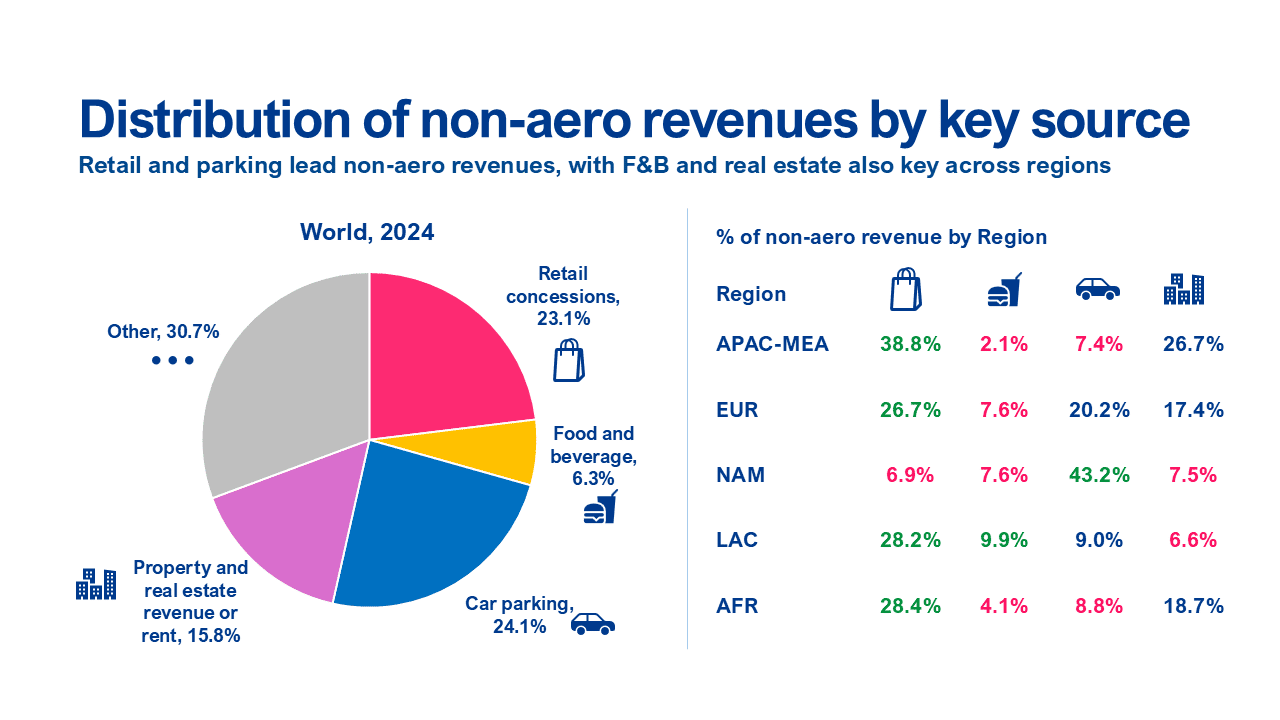

Airport Commercial Revenue Structure Shapes Revenue Outcomes

Globally, non-aeronautical revenues remain concentrated in a limited number of core segments, largely driven by the weight of North America in car parking revenues.

Key contributors include:

- Car parking: 24.1% of global non-aeronautical income

- Retail concessions: 23.1%

- Property and real estate: 15.8%

- Food and beverage: 6.3%

Retail concessions remain the largest source of non-aeronautical revenue across all regions except North America. In North America, parking accounts for 43.2% of non-aeronautical revenues. By contrast, in APAC–MEA retail represents 38.8%, and in Europe retail stands at 26.7%, supported by a significant contribution from property revenues.

The regional distribution reflects differing commercial structures across markets.

Key Statistics on Airport Non-Aeronautical Revenues

- Global passenger traffic: ~4% above 2019 levels

- Non-aeronautical revenues: ~9% below 2019 levels globally

- Share of airport income: 36.7% of total airport revenues

- Cost recovery: offset 48% of total airport costs

- Average non-aeronautical revenue per passenger: USD 7.57

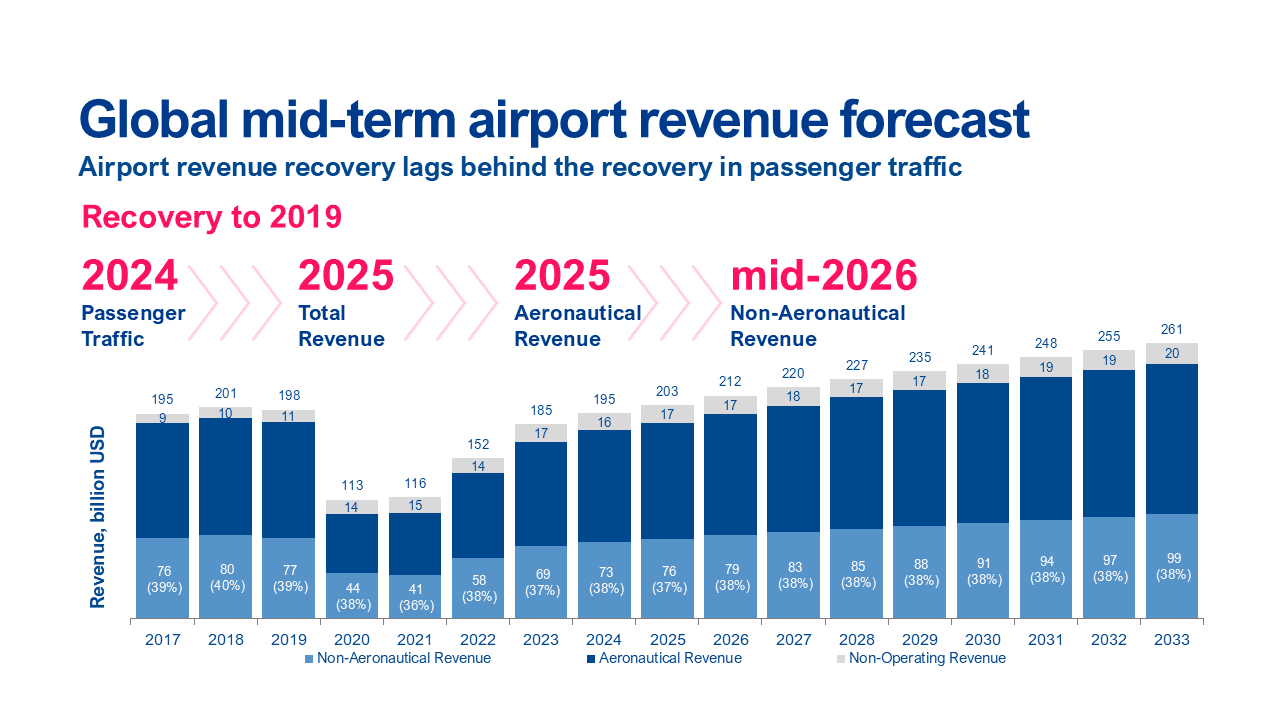

The Mid-Term Outlook for Airport Revenues

ACI World’s mid-term airport revenue forecast through 2033 assumes continued steady passenger growth alongside a further decline in non-aeronautical revenue per passenger. Under this scenario, total non-aeronautical revenues are projected to grow at around 3% CAGR, increasing from USD 73 billion in 2024 to approximately USD 99 billion in 2033. Growth is therefore expected to be driven primarily by volume rather than yield.

The sequencing of recovery remains clear:

- Passenger traffic recovery: 2024

- Total airport revenue recovery: expected in 2025

- Non-aeronautical revenue recovery: projected between mid-2026 to 2027

This implies a lag of roughly two and a half years between traffic recovery and non-aeronautical revenues recovery.

Megatrends Shaping the Future of Airport Non-Aeronautical Business

Discussions among industry leaders at The Trinity Forum 2026, the world’s leading airport commercial revenues and travel retail gathering, highlight several megatrends shaping the future of airport commercial strategy.

Megatrend 1. Experience is becoming central to commercial success.

Airport retail is evolving from transactional models toward immersive experience-led environments. Lounges, cultural storytelling, and sense of place are increasingly driving engagement and spend.

Megatrend 2. Ecosystem collaboration is a competitive advantage.

Stronger alignment across airports, airlines, brands, concessionaires, and media partners is emerging as a key enabler of innovation and sustainable commercial growth.

Megatrend 3. Local identity as a differentiator.

Embedding local culture, heritage, and identity into retail and F&B concepts strengthens passenger connection and commercial performance.

Megatrend 4. Generational shifts in traveller behaviour

Generational shifts in traveller behaviour are reshaping expectations around digital engagement, consumption patterns and brand alignment.

These megatrends will shape the trajectory of revenue per passenger and airport commercial models in the years ahead.

Key Takeaways: From Passenger Traffic Recovery to Commercial Value Reinvention

Passenger traffic has recovered and long-term demand remains strong. Yet:

- Total airport revenues remain slightly below 2019 levels globally

- Non-aeronautical revenues continue to trail pre-pandemic benchmarks

- Revenue per passenger remains under pressure across most regions.

The implication is structural. While passenger traffic volumes have returned, the airport commercial landscape has fundamentally changed. There will be no return to pre-2019 business models or to business as usual.

Airports – together with their partners – must now actively shape what comes next through new non-aeronautical strategies.

For More Insights

Access the newly-released ACI World 2026 Airport Economics Report and Key Performance Indicators, drawing on financial year 2024 data from more than 1,000 airports of all sizes and business models — representing approximately 82% of global passenger traffic.

This analysis builds on the work of the ACI World Airports Non-Aeronautical Revenues and Activities (ANARA) Specialized Group, which brings together airports and industry partners to examine trends shaping airport commercial performance and non-aeronautical revenues worldwide.

Sources

- Airports Council International (ACI) World. Airport Economics Report and Key Performance Indicators 2025. Montreal: ACI World, 2025.

- Airports Council International (ACI) World. World Airport Traffic Report 2024. Montreal: ACI World, 2025.

- Airports Council International (ACI) World. World Airport Traffic Forecasts 2025–2054. Montreal: ACI World, 2026.

ROCIO

24 Jun 2026

Excelente informe apreciado amigo.